Indian Ice Manufacturing Industry

Global Market Overview

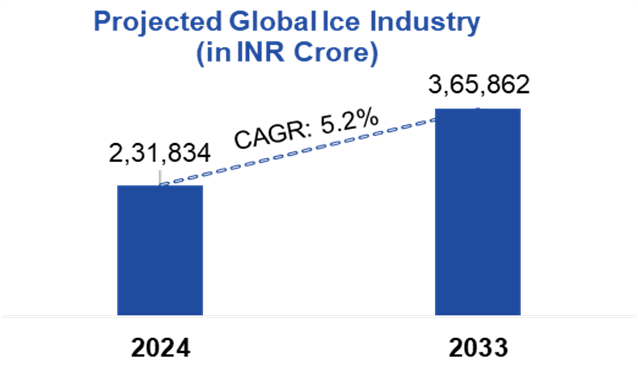

The global ice market was valued at approximately INR 2.31 lakh crore (USD 25.6 billion) in 2024 and is projected to reach INR 3.65 lakh crore (USD 40.4 billion) by 2033, growing at a CAGR of 5.2%.1

The market includes multiple product categories such as3:

- Ice cubes

- Ice flakes

- Ice nuggets

- Block ice

- Tube ice

- Specialty packaged ice

These products are distributed through supermarkets, convenience stores, online retail channels, foodservice suppliers, healthcare providers, and industrial distributors.

Demand Drivers:

- Rising consumption of beverages globally

- Growth in food delivery and hospitality industries

- Increasing cold-chain requirements

- Higher healthcare usage for temperature-sensitive transportation

- Sustainability-led innovation in manufacturing processes

Asia-Pacific is expected to be one of the fastest-growing regions due to rising urbanization, industrial expansion, and increasing middle-class consumption.

Key Global Players

Major global players in the ice manufacturing industry include:

- Cornelius Inc.

- Minnesota Ice

- Arctic Glacier

- Genesee Ice

- The Ice Co

Indian Ice Market

India’s ice manufacturing industry is currently valued at over INR 10,000 crore (USD ~1.1 billion) in 2025, with projected annual growth of approximately 10–12%2.

As temperatures continue to rise and industrial demand expands, India’s ice manufacturing sector is witnessing steady growth.

The industry plays a critical role across sectors such as:

- Hospitality

- Food service

- Fisheries

- Healthcare

- Logistics

- Retail cooling

- Beverage distribution

The industry remains highly fragmented, with a large portion of the market still dominated by regional operators.

There are approximately 4,789 ice suppliers in India as of November 2025. Maharashtra alone accounts for nearly 9.7% of total ice suppliers in India.4

Key Players in India

- Icelings

- HP Ice Blocks Factory

- Paul Coldice Industries

- Rock Ice

Growth Drivers

Rising Temperature Trends

Increasing temperatures across India are driving year-round demand for commercial and retail ice consumption.

Foodservice Expansion

Growth in restaurants, quick-service restaurants, cloud kitchens, and beverage chains is significantly increasing demand.

Fisheries & Seafood Demand

Ice remains critical for fish preservation and transportation.

Cold Chain Expansion

India’s cold-chain ecosystem is improving rapidly, increasing demand for reliable ice production5.

Low Entry Barriers

The industry typically requires moderate capital expenditure and has relatively simple operational models.

Organized Market Growth

While over 90% of India’s cold-chain market remains unorganized, organized players are expanding rapidly to meet hygiene and scalability requirements.

Ice Cube Market

The global ice cube market is expected to grow from INR 25,266 crore (USD 2.79 billion) in 2026 to INR 40,833 crore (USD 4.51 billion) by 2035, growing at a CAGR of 3.7%.6

Ice cubes remain one of the most widely consumed formats due to demand from:

- Restaurants

- Cafes

- Bars

- Hotels

- Convenience retail

- Household consumption

North America currently holds the largest market share, while Asia-Pacific is expected to witness the fastest growth.

Ice Pops / Chuski Market

The global ice pops market was valued at approximately INR 47,635 crore (USD 5.26 billion) in 2024 and is projected to grow at a CAGR of 7.2% through 2030.7

Ice pops (also known as freezer pops/ice lollies) are gaining popularity due to:

- Rising disposable incomes

- Demand for affordable frozen treats

- Product innovation

- Health-focused flavor offerings

- Convenience-driven consumption patterns

Major FMCG Players in Ice Pops

- Unilever

- Nestlé

- Amul

- Mother Dairy

- Kwality Wall's

Emerging Players

- Skippi Ice Pops

Key Industry Segments

Commercial Ice

- Restaurants

- Hotels

- Bars

- Catering businesses

- Retail chains

Industrial Ice

- Fisheries

- Food processing

- Pharmaceutical transportation

- Logistics

Retail Packaged Ice

- Growing rapidly in urban convenience stores and supermarkets.

Frozen Dessert Ice Products

- Includes ice pops, flavored ice products, and impulse frozen treats.

Government Initiatives

Pradhan Mantri Matsya Sampada Yojana (PMMSY)

Introduced by the Ministry of Fisheries, Animal Husbandry and Dairying, this initiative supports cold storage and ice plant development.8

The scheme provides:

- Financial assistance for setting up 20-ton capacity ice plants

- Cold storage infrastructure support

- Fish preservation support

Funding Model:

- 50% Central Government

- 50% State Government

Integrated Cold Chain and Value Addition Infrastructure (ICCVAI)

Implemented by the Ministry of Food Processing Industries, this program focuses on strengthening India’s end-to-end cold chain infrastructure.9

The initiative helps:

- Reduce post-harvest losses

- Improve farmer income realization

- Strengthen food distribution efficiency

- Improve perishables logistics

Mergers & Acquisitions

Arctic Glacier Acquisition (2017)

The Carlyle Group acquired Arctic Glacier from H.I.G. Capital for approximately USD 723 million (INR 6,547 crore).10

Reddy Ice Acquisition (2020)

Stone Canyon Industries acquired Reddy Ice for approximately USD 425 million (INR 3,849 crore).11

Manitowoc Ice Acquisition (2022)

Pentair plc acquired Manitowoc Ice for approximately USD 1.6 billion (INR 14,490 crore).12

Industry Outlook

The Indian ice manufacturing sector presents strong long-term potential due to:

- Rising temperatures

- Expanding foodservice demand

- Growth in fisheries and seafood logistics

- Rapid cold-chain infrastructure development

- Increasing demand for hygienic packaged ice

- Growing frozen dessert consumption

Despite being highly fragmented today, the industry is gradually shifting toward organized, scalable, and branded players—creating meaningful opportunities for consolidation and institutional investment.

Porter’s 5 Force Analysis

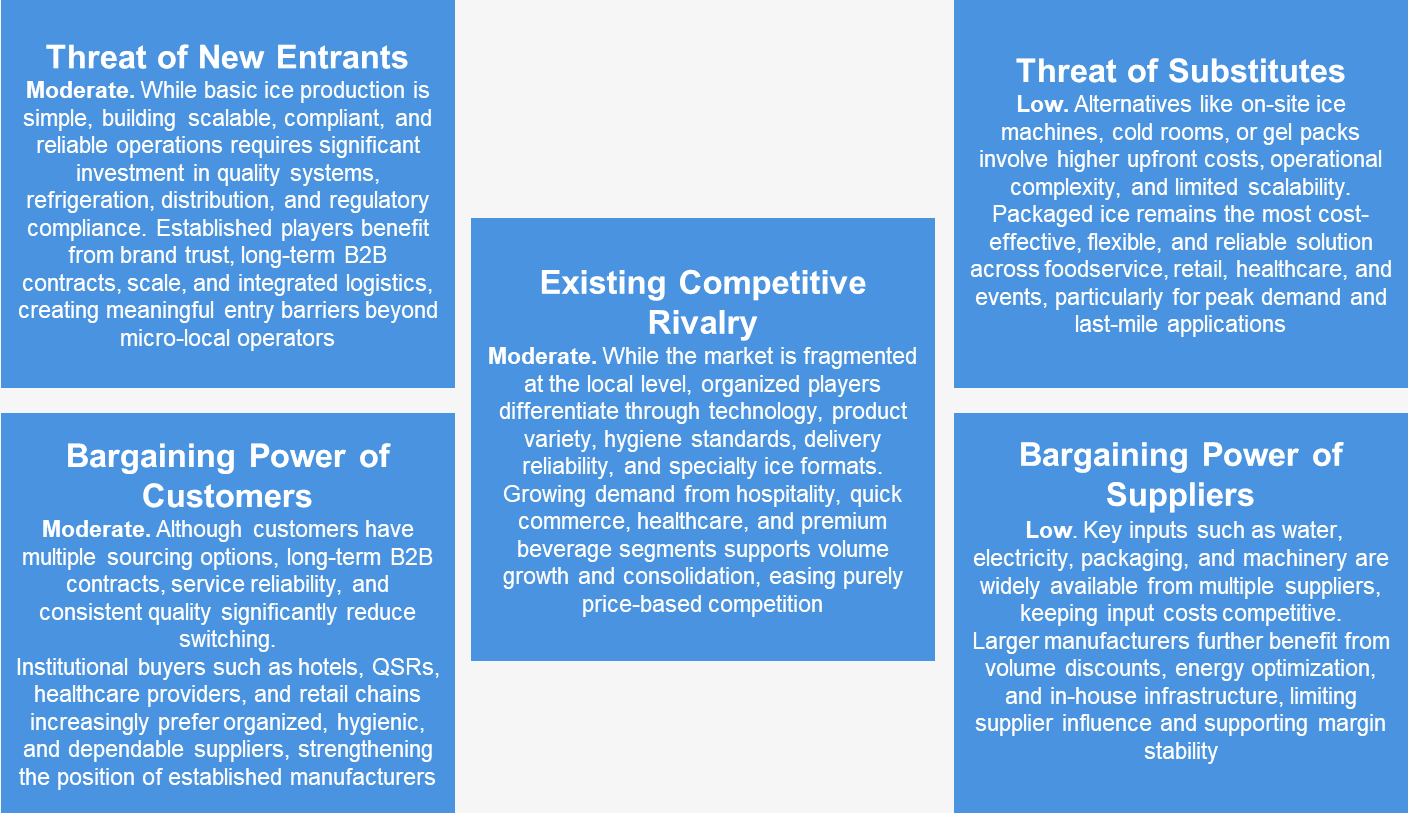

Threat of New Entrants – Moderate

While basic ice production is simple, building scalable, compliant, and reliable operations requires significant investment in quality systems, refrigeration, distribution, and regulatory compliance. Established players benefit from brand trust, long-term B2B contracts, scale, and integrated logistics, creating meaningful entry barriers beyond micro-local operators.

Threat of Substitutes – Low

Alternatives like on-site ice machines, cold rooms, or gel packs involve higher upfront costs, operational complexity, and limited scalability. Packaged ice remains the most cost-effective, flexible, and reliable solution across foodservice, retail, healthcare, and events, particularly for peak demand and last-mile applications.

Bargaining Power of Customers – Moderate

Although customers have multiple sourcing options, long-term B2B contracts, service reliability, and consistent quality significantly reduce switching. Institutional buyers such as hotels, QSRs, healthcare providers, and retail chains increasingly prefer organized, hygienic, and dependable suppliers, strengthening the position of established manufacturers.

Bargaining Power of Suppliers – Low

Key inputs such as water, electricity, packaging, and machinery are widely available from multiple suppliers, keeping input costs competitive. Larger manufacturers further benefit from volume discounts, energy optimization, and in-house infrastructure, limiting supplier influence and supporting margin stability.

Existing Competitive Rivalry – Moderate

While the market is fragmented at the local level, organized players differentiate through technology, product variety, hygiene standards, delivery reliability, and specialty ice formats. Growing demand from hospitality, quick commerce, healthcare, and premium beverage segments supports volume growth and consolidation, easing purely price-based competition.

Trading Comparables

| Trading Comparables | |||||

| (In INR crore, As on 31st December 2025) | Enterprise Value (EV) | Revenue (TTM) | EBITDA | EV / Revenue | EV / EBITDA |

| Company | |||||

Vadilal Industries Limited13 |

3,617 |

1,335 |

213 |

2.7x |

17.0x |

Ice Make Refrigeration Limited14 |

1,439 |

550 |

41 |

2.6x |

34.8x |

Dodla Dairy Limited15 |

6,918 |

3,837 |

354 |

1.8x |

19.5x |

Heritage Foods Limited16 |

4,051 |

4,332 |

303 |

0.9x |

13.4x |

Transaction Comparables:

| Transaction Comparables | |||||

| Target Description | Target | Acquirer / Investor | EV (in INR Cr) | EV/ Revenue | EV/ EBITDA |

| October, 2025 : Get-A-Way is an Indian healthy dessert brand, specializing in high-protein, low-calorie, zero-added-sugar ice creams and treats | Get-A-Way (Peanut butter And Jelly Private Limited)17 |

Heritage Foods |

17.65 |

1.0x |

NA |

| September, 2025 : Hocco is an ice cream brand offering authentic experiences at dining restaurants, quick-service eateries, and ice cream cafes. | Hocco18 |

Sauce VC |

2,000 |

9.1x |

NA |

| August, 2024 : Cheney Brothers is a family owned and operated broadline distributor offering over 64,000 stocked items from gourmet to everyday. Cheney EXPRESS is open to the public and carries frozen, refrigerated and dry products with carry out service. | Cheney Brothers19 |

Performance Food Group |

18,862 |

0.7x |

13.0x |

Sources

- Global Ice Market

- Indian Ice Market

- Ice Market Size, Share & Trends Analysis Report

- Ice Suppliers in India

- India Cold Chain Market Report

- Ice Cube Market Size Report

- Ice Pop Market Report

- PMMSY

- ICCVAI

- Arctic Glacier Acquisition

- Reddy Ice Acquisition

- Manitowoc Ice Acquisition

- Vadilal Industries Limited

- Ice Make Refrigeration Limited

- Dodla Dairy Limited

- Heritage Foods Limited

- Get-A-Way (Peanutbutter And Jelly Private Limited)

- Hocco

- Cheney Brothers