Indian Water and Wastewater Treatment Industry

The Indian water and wastewater treatment industry is a regulation-driven infrastructure and environmental services sector that supports municipal bodies, industrial facilities, utilities, and urban development authorities with water purification, wastewater recycling, desalination, sludge management, and reuse solutions. The sector is being shaped by rising water stress, urbanization, industrialization, stricter discharge norms, and government-led investments in drinking water and sewage infrastructure.

India’s water and wastewater treatment market is projected to reach approximately INR 2.1 lakh crore (USD 23.8 billion) by 2033, growing from INR 1.15 lakh crore (USD 13.1 billion) in 2023 at a CAGR of ~6.2%.1p.22

The industry supports municipal corporations, industrial zones, residential townships, utilities, and commercial infrastructure projects through a broad range of treatment, recycling, and water-management solutions.

Key Industry Highlights

- India accounts for nearly 18% of the world’s population but has access to only around 4% of global freshwater resources, creating long-term structural demand for water treatment and recycling infrastructure2p.2

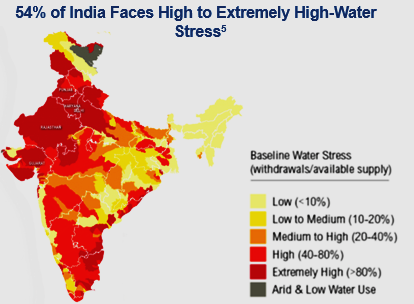

- Around 54% of India faces high to extremely high water stress, increasing the urgency for water reuse, conservation, and wastewater treatment investments5

- Water demand in India is expected to rise from approximately 710 BCM in 2010 to nearly 1,180 BCM by 2050, with industrial and domestic water consumption expected to increase significantly1p.26

- Agriculture consumes over 91% of India’s freshwater withdrawals, creating opportunities for treated wastewater reuse and efficient irrigation systems4.s6

- Only about 28% of India’s sewage is currently treated, while untreated wastewater continues to contaminate rivers, lakes, and groundwater reserves1p.26

- India aims to achieve 25% wastewater reuse by 2026 and nearly 50% reuse by 2050, supporting long-term investments in tertiary treatment, recycling, and ZLD systems1p.26

- More than 500 new treatment plants are planned by 2027, adding roughly 20 billion liters per day (BLD) of treatment capacity across urban and industrial regions2p.3

- Public-Private Partnership (PPP) participation under AMRUT 2.0 and other schemes is creating opportunities for EPC contractors, technology providers, equipment manufacturers, automation vendors, and O&M service companies

Market Drivers

1. Rising Water Scarcity and Urbanization

Rapid urbanization and population growth are increasing pressure on India’s limited freshwater resources. India’s urban population is projected to require nearly 1,450 km³ of water by 20501p.26, driving investments in drinking water, wastewater recycling, and decentralized treatment systems.

2. Government Infrastructure Spending

Large-scale government initiatives including Jal Jeevan Mission (JJM), AMRUT 2.0, Namami Gange, and Atal Bhujal Yojana are significantly increasing public expenditure on water supply, sewage networks, groundwater management, and smart water infrastructure.

3. Industrial Compliance Requirements

Industries such as textiles, chemicals, pharmaceuticals, food processing, and power generation are increasingly adopting advanced treatment and ZLD systems to comply with stricter pollution control norms and water reuse mandates.

4. Growing Wastewater Reuse Focus

Municipal bodies and industrial facilities are increasingly adopting treated wastewater reuse for industrial cooling, landscaping, construction, and agriculture to reduce freshwater dependency.

5. Technology Adoption and Smart Water Management

The sector is witnessing increasing adoption of membrane bioreactors (MBR), reverse osmosis (RO), IoT-enabled monitoring systems, SCADA-based automation, AI-driven leak detection, and advanced sludge treatment technologies.

India Wastewater Treatment Scenario

India’s wastewater management ecosystem remains significantly underpenetrated despite rising contamination risks and increasing regulatory pressure. Most Indian cities still discharge untreated or partially treated wastewater into rivers and groundwater bodies, creating a major environmental and public health challenge.

The wastewater treatment market is increasingly shifting toward reuse-focused solutions, including tertiary treatment, industrial recycling, and Zero Liquid Discharge (ZLD) systems.

Key Demand Drivers for Chemically Treated Wastewater

Municipal Segment

- Increasing urban sewage generation

- Expansion of sewerage infrastructure in Tier-1 and Tier-2 cities

- Smart city and river-cleaning initiatives

Industrial Segment

- Mandatory compliance with discharge norms

- Water-intensive industries adopting ZLD systems

- Rising penalties for non-compliance

Agriculture and Reuse

- Treated wastewater increasingly being used for irrigation

- Circular economy initiatives promoting water reuse

- Rising awareness around sustainable water management

Household and Drinking Water Demand

- Growing concerns regarding groundwater contamination

- Rising demand for safe drinking water and purification systems

- Investments in decentralized treatment infrastructure

Conventional ETP vs Zero Liquid Discharge (ZLD)

| Parameter | Conventional ETP | Zero Liquid Discharge (ZLD) |

|---|---|---|

Final Output |

Treated water discharged |

Recycled water and solid waste |

Water Recovery |

~70% or lower |

95–99% |

Discharge |

Sewer, drain, or river |

No liquid discharge |

Sludge Handling |

Often secondary priority |

Core part of process |

Compliance Risk |

Moderate to High |

Minimal |

Sustainability |

Lower |

Significantly higher |

ZLD adoption is increasing rapidly across textile, pharmaceutical, chemical, and power-generation industries due to tightening environmental regulations and long-term freshwater conservation requirements.

Government Initiatives and Schemes

Jal Jeevan Mission (JJM)

Focus Area

Rural drinking water infrastructure.

Objective

Provide Functional Household Tap Connections (FHTC) to every rural household.

Estimated Outlay

Approximately INR 3.6 lakh crore with enhanced annual allocations.

Key Opportunities

- Rural pipeline infrastructure

- Water quality monitoring

- Decentralized treatment systems

- Operations & Maintenance (O&M) services

Industry Impact

States with lower rural water coverage continue to present strong EPC and infrastructure opportunities, while mature states are transitioning toward O&M and technology-upgrade markets.

AMRUT 2.0

Focus Area

Urban water supply and sewerage management.

Estimated Outlay

Approximately INR 2.99 lakh crore.

Key Opportunities

- Sewage treatment plants (STPs)

- Smart water management systems

- SCADA automation

- Public-Private Partnership (PPP)-based infrastructure projects

Industry Impact

High-value urban projects are concentrated in states such as Maharashtra, Uttar Pradesh, Tamil Nadu, and Karnataka.

Atal Bhujal Yojana (ATAL JAL)

Focus Area

Groundwater sustainability and conservation.

Estimated Outlay

Approximately INR 6,000 crore.

Key Opportunities

- Water efficiency technologies

- Data analytics and groundwater monitoring

- Demand-side water management solutions

Geographic Scope

Focused on water-stressed rural regions across seven states.

Porter’s Five Forces Analysis

Threat of New Entrants – Low

The sector requires significant capital investment, strong technical expertise, regulatory approvals, and proven execution capabilities. Established players benefit from long-standing government relationships, execution track records, and integrated EPC capabilities.

Threat of Substitutes – Low

Water and wastewater treatment infrastructure remains essential with limited substitutes. Alternative technologies may optimize treatment processes but cannot eliminate the need for treatment itself.

Bargaining Power of Customers – Medium to High

Government tenders and industrial procurement are highly price-sensitive and competitive. Large buyers possess strong negotiating power, particularly in standardized EPC contracts.

Bargaining Power of Suppliers – Low

Most raw materials such as steel, cement, pipes, pumps, and chemicals are commoditized with multiple suppliers available, limiting supplier influence.

Existing Competitive Rivalry – Medium

The market is highly fragmented, with competition among global water technology firms, domestic EPC contractors, equipment manufacturers, and specialized regional players. Differentiation is increasingly driven by technology, execution capability, lifecycle O&M services, and integrated water management solutions.

Industry Outlook

India’s water and wastewater treatment industry is expected to witness long- term structural growth driven by worsening water scarcity, rising urbanization, industrial expansion, stricter environmental regulations, and large-scale public infrastructure investments.

Increasing adoption of wastewater recycling, smart water systems, and ZLD technologies is expected to create significant opportunities for EPC companies, technology providers, automation firms, equipment manufacturers, and infrastructure investors over the next decade.

The sector is evolving from a basic treatment-focused industry toward an integrated water management ecosystem centred on sustainability, reuse, digital monitoring, and circular water economy models.

Transaction Comparables (in INR Cr)

| Date | Target | Acquirer / Investor | Target Description | EV | EV / Revenue | EV / EBITDA |

Sep-07 |

Gondwana Engineers 6 |

Kirloskar Brothers Ltd |

Gondwana specialises in the construction of various water, sewage, and effluent treatment plants. |

766 |

0.2x |

N/A |

Apr-16 |

Shriram EPC 7 |

Mark AB Capital |

EPC company focused on providing integrated turnkey solutions for water and wastewater treatment plants, water & sewer systems, biomass-based power plants, mini hydel plants, process and metallurgy plants. |

1,32,175 |

2.4x |

N/A |

Nov-24 |

Pureit (Water Purification Business of Hindustan Unilever Ltd.) 8 |

AO Smith India Water Products Pvt. Ltd. |

AO Smith acquired Hindustan Unilever’s Pureit water purification business, including trademarks, IP, and associated assets. |

601 |

2.1x |

N/A |

| Median | 2.1x |

Trading Comparables (In INR Crore, As on 3 October 2025)

| Company | Enterprise Value (EV) | Revenue (TTM) | EBITDA (TTM) | EV / Revenue | EV / EBITDA |

Thermax Limited (THERMAX.NS) 9 |

34,928 |

10,354 |

972 |

3.4x |

35.9x |

Enviro Infra Engineers Ltd (EIEL.NS) 10 |

4,249 |

1,102 |

280 |

3.9x |

15.2x |

Ion Exchange (India) Limited (IONEXCHANG.NS) 11 |

5,071 |

2,753 |

295 |

1.8x |

17.2x |

VA Tech Wabag Limited (WABAG.NS) 12 |

8,341 |

3,402 |

440 |

2.5x |

19.0x |

| Median | 2.9x | 18.1x |

Sources:

- Denta Water and Infra Solutions Limited – Annual Report 2024-25

- Water Industry Thematic Report: Unlocking Blue Revolution (2025)

- AMRUT 2.0 Operational Guidelines

- Water Use Efficiency – Ministry of Water Resources

- World Economic Forum Water Sector Article

- Kirloskar Brothers buys Gondwana Engineers

- Mark AB Capital becomes promoter of SEPC

- AO Smith completes acquisition of Pureit

- Thermax Limited

- Enviro Infra Engineers Ltd

- Ion Exchange (India) Limited

- VA Tech Wabag Limited